Why you should invest in MF schemes investing overseas?

Investors must understand the associated risks before investing into them. An

allocation of 10% to the global funds may be preferred.

Choppy equity markets and spurting bond yields in the recent weeks in the domestic market should not materially alter the long term asset allocation levels. But these events do serve as a good reminder to diversify the domestic portfolio. In India, the major asset classes that offer easy tradability are listed equity, fixed income, gold through ETFs and commodities to some extent. This diversification alone may not be enough given that Indian market is increasingly being impacted by global events over and above the domestic ones. Globally, different economies are driven by internal growth factors and respond differently to major events. The stability in the equity market of a developed economy can cushion the high volatility seen in an emerging market like ours.

Investors must understand the associated risks before investing into them. An

allocation of 10% to the global funds may be preferred.

Choppy equity markets and spurting bond yields in the recent weeks in the domestic market should not materially alter the long term asset allocation levels. But these events do serve as a good reminder to diversify the domestic portfolio. In India, the major asset classes that offer easy tradability are listed equity, fixed income, gold through ETFs and commodities to some extent. This diversification alone may not be enough given that Indian market is increasingly being impacted by global events over and above the domestic ones. Globally, different economies are driven by internal growth factors and respond differently to major events. The stability in the equity market of a developed economy can cushion the high volatility seen in an emerging market like ours.

Indian investors can invest in overseas assets through the liberalized remittance scheme (LRS) which allows up to $125000 (proposed $250,000) per annum. A simpler route is through domestic mutual funds that offer exposure to global equities either by feeding into an existing offshore fund or investing directly into overseas equities. The mutual fund route doesn’t come under the purview of LRS.

Over a period of time with wealth managers acknowledging the need of geographical diversification, mutual funds have launched plethora of funds providing exposure to global equities . The universe of feeder funds offers geographical diversification as well as interesting themes. The funds may target specific region like US, Europe, Asia, Latin America, a combination of developed regions or emerging markets in general. The funds also tap sections of the region like periphery of Europe or Value / Growth companies in the US. Global thematic funds offer new opportunities for Indian investors to tap specific segments in the global markets. Themes currently available include commodities, bullion, oil, real assets, real estate, mining and agriculture. These options are not otherwise available as investment vehicles in India due to lack of a tradable market for these assets or regulatory restrictions in India.

Investment in overseas tradable assets is considered as non-domestic equity and attracts fixed income taxation of 20% with indexation. Hence some mutual funds maintain a minimum of 65% in domestic equity and deploy the rest in the overseas fund to qualify for equity taxation. But, diversification of the domestic portfolio being the primary criterion for inclusion of overseas equity, a heavy tilt towards domestic equities in a global fund will dilute the essence of diversification. Hence, we would prefer funds that offer unhindered 100% participation in overseas equities.

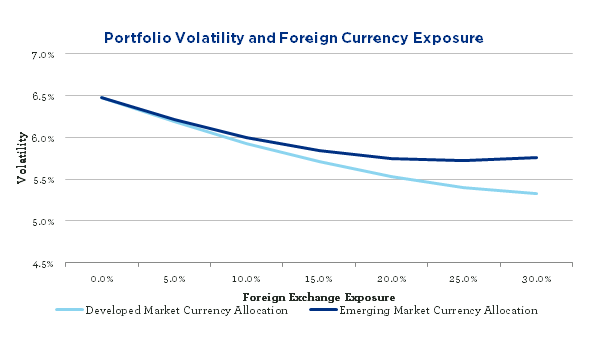

Funds focusing on a single region expose the investor to higher levels of country specific risks and currency fluctuations. For optimal diversification, investors may consider feeder funds that provide non-concentrated exposure to top few regions rather than a single country. For example, if India displays risk-return characteristics similar to those of other emerging economies then global events would have comparable impact on India and other emerging economies. In such a situation, investing in a global emerging market fund will not serve the purpose as most emerging economies are highly correlated. Instead, looking at a fund that invests in a bunch of less correlated developed economies can counterbalance the domestic market volatility to some extent.

Some other key points to consider

• Feeder fund route Versus direct overseas equity fund

The underlying parent funds of Feeder funds usually have a long and a proven performance and fund management track record as compared to Indian domestic funds investing directly in overseas equity which seek advisory from the overseas fund managers. Expense-wise, all the funds are bound to follow the same upper limit prescribed by SEBI. This upper limit for expense should include charges by parent and feeder fund.

• Investment Tenure

Positive effect of Rupee depreciation further adds to the returns made by global funds. This effect is experienced over the medium term. Also, equity as an asset class requires a medium to long term horizon to see meaningful returns. An investment horizon of at least three years should be preferred for these investments. Overseas equity is treated as non-domestic equity investment in India for taxation and thus attracts debt taxation. Having a 3-year horizon will also help benefit from long term debt taxation of 20% with indexation.

• Risks

Region-specific risks can be handled by the way of geographical diversification. But at times, major global events have the propensity to affect all global economies and commodities in similar fashion. In case of a catastrophic event where all markets behave likewise, the essence of global diversification will be lost. Another risk is posed by currency movement. Returns from global mutual funds have two parts – performance of the underlying market/ parent fund and domestic currency movement (investor’s home currency). An appreciating rupee over a period of time can shave off some gains from such funds for the domestic investor.

In conclusion, investors must fully understand the nature of the global funds and the associated risks before investing into them. An allocation of 10% to the global funds may be preferred. Investors may choose global feeder funds with multiple underlying regions that are less correlated with each other and with the Indian markets. Within themes, investors may pick up those that are sustainable for a longer time period like agriculture rather than a transiting or cyclical trend.

Source - moneycontrol.com

Source - moneycontrol.com